The Stakeholder Theory is a theory of organizational management that states that companies could archive better performance by taking all stakeholders into account, not only shareholders. Stakeholders are clients, suppliers, employees, the government and the society where the company operates.

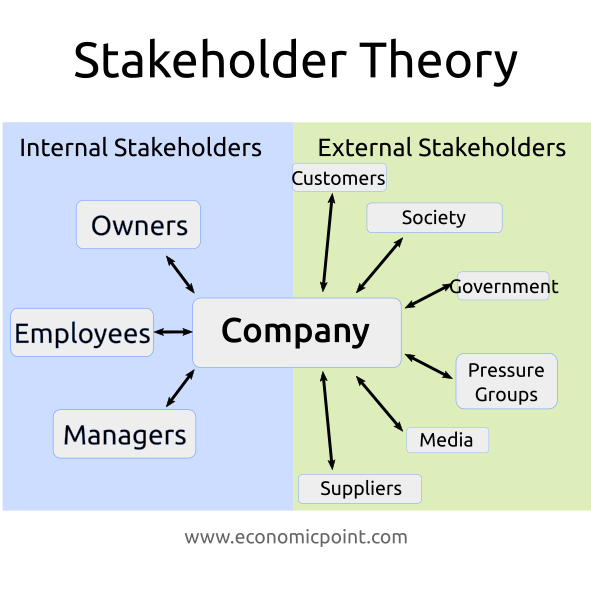

Stakeholders are defined as parties that are affected by the actions of the company, directly or indirectly. Stakeholders can be classified in internal and external.

Internal stakeholders are:

- Owners

- Employees

- Managers

External stakeholders are:

- Suppliers

- Customers

- Society

- Government

Edward Freeman developed the Stakeholder Theory in his classical book Strategic Management: A Stakeholder Approach (Freeman, 1984).

Freeman argues that traditional management theories, that only take shareholders interest into account, are not suited for the modern global economy, characterized by rapid technological change, new industrial relations, increased globalization and increasing influence by pressure groups.

The Stakeholder Theory quickly gained interest, but also detractors. One of the main issues of the theory is that many interpreted it as a managerial theory that mixes business with moral appeals. Another important critic of the theory is that it difficults risk-taking and corporate governance.

Shareholders vs Stakeholders Debate

From the economic point of view, the Stakeholder Theory represents a departure from neoclassical economics.

Milton Friedman, a renowned economist, suggest that managers should only take the shareholders interest into account. Shareholders should decide by themselves what social actions should be carried by the company. Two schools of thought on the subject formed.

(1) Edward Freeman, 1984: Strategic Management: A Stakeholder Approach, Pitman, 1984 ISBN 0273019139